Received 25 July 2022; Revised 12 September 2022; Accepted 20 September 2022.

This is an open access paper under the CC BY license (https://creativecommons.org/licenses/by/4.0/legalcode).

Szczepan Kościółek, PhD., Research and Teaching Assistant, Faculty of Management and Social Communication, Jagiellonian University in Krakow, Poland, Instytut Przedsiebiorczosci UJ, Lojasiewicza 4, 30-348 Krakow, Poland, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

Abstract

PURPOSE: As the issue of the motivations of crowdinvestors is still heavily debated, empirical research has come to focus on specific industries and the heterogeneity of motivations within specific crowdfunding models. This study combines these two perspectives and considers the research question of the heterogeneous motivations of football club crowdinvestors. The aim of the study is to segment the football club crowdinvestors according to investment motivations. METHODOLOGY: In this study, the survey research method was used for a sample (n = 793) of crowdinvestors from the Wisla Krakow football club, and a two-step motivation-based segmentation approach was applied. The convenient sampling method was used as the club distributed the surveys electronically among all its crowdinvestors in July 2021. A cluster analysis, including Ward’s method with Euclidian distance and the non-parametric k-means method, was applied to segment the market. Differences between segments were assessed with chi-square tests for qualitative variables and Kruskal-Wallis H tests with Dunn’s post hoc tests for quantitative variables. A discriminant analysis successfully validated the segmenting procedure. FINDINGS: The crowdinvestors of football clubs were divided into three market segments: benefit-oriented (50.7%), club-oriented (45.3%), and goal-oriented (4.0%). This clustering solution was influenced by all of the previously identified motivations: fan identification, supporting a campaign’s cause, status of football club owner, rewards, and return on investment. The segments were also differentiated according to consumption-related behaviors (media consumption, word-of-mouth marketing, merchandise purchases, match attendance, and social media engagement) and socio-demographic profiles (age, marital status, income, and place of residence). With the exception of the goal-oriented niche, crowdinvestors of football clubs are fans who are highly identified with the club and focused on supporting the cause of the campaign. However, some of them (“benefit-oriented”) are more sensitive than others to the return on investment, rewards, and status that comes along with club ownership (“club-oriented”). Benefit-oriented crowdinvestors consume the club’s products to the greatest extent, while goal-oriented crowdinvestors are on the opposite side of the spectrum. IMPLICATIONS: Based on self-determination theory, no cluster with a predominance of extrinsic motivations was found. These results are in opposition to most crowdfunding studies, but are in line with sport management literature. Importantly, evidence was found showing that groups that are homogenous in terms of crowdinvestment activity can still be heterogeneous in terms of crowdinvestment motivations. This insight shows that crowdinvestment motivations should be considered in more detail than they have been in the past. The assumptions of the multi-needs-meeting phenomenon of crowdinvesting in football clubs were also confirmed. These outcomes provide sports managers with information about market segments of crowdinvestors that they can use to communicate their crowdfunding campaigns more effectively. ORIGINALITY AND VALUE: This study is the first to present the research-tested heterogeneity of investment motivations among football club crowdinvestors. It shows the instability of research results that focus on entire crowdfunding models and ignore the industry-related specificities and internal diversity of crowdinvestors. Moreover, it extends the area of research on fan investors in the football industry, which has, until this point, focused on investment motivations without taking their internal heterogeneity into account.

Keywords: equity crowdfunding, fans investors, market segmentation, self-determination theory (SDT), sports clubs, team identification.

INTRODUCTION

Crowdfunding has partially filled the capital gap faced by small and micro-sized enterprises, particularly start-ups, which find it challenging to have their projects funded by traditional sources such as bank loans, venture capitalists, or their own savings (Gierczak et al., 2016). By financing risky technological projects as well as ambitious cultural and social ventures, crowdfunding has created a market that is estimated to reach USD 1.3 billion by 2028 (Bloomberg, 2022). What is less obvious is that interest in crowdfunding is also growing immensely among sports managers of professional European football clubs (Huth, 2018a, 2018b), who have to face the structural problem of financial instability of the units managed by them (Ahtiainen & Jarva, 2022; Nessel, Havran, & Máté, 2022; Perechuda, 2020).

Football clubs with fans’ crowds perfectly fit the opportunities offered by the crowdfunding ecosystem, which is based on the acquisition of funds for projects by means of amassing usually small amounts from a number of persons, chiefly via electronic trading platforms (Belleflamme, Lambert, & Schwienbacher, 2014). In contrast to technological start-ups, traditionally considered the main beneficiaries of crowdfunding (Kozioł-Nadolna, 2016; Leboeuf & Schwienbacher, 2018), football clubs have the advantage of a recognizable brand for an existing group of customers to whom they can easily target their campaigns. However, considering the specificity of sports consumers’ behavior (Mullin, Hardy, & Sutton, 2014), the investment behaviors of this particular group differ from those of other sectors (Huth, 2020; Prigge & Tegtmeier, 2020; Weimar & Fox, 2021). It turns out that the fans investors, the main target group for football club shares, are primarily motivated intrinsically by the psychological connection to the sport entity they support without expecting profitable financial returns. Therefore, their motivations for crowdfunding are also the subject of separate studies (Kościółek, 2021, in press). As with other forms of investment, it was noticed that football clubs’ campaigns mainly attracted their fans, who were motivated primarily by the will to support “their” team and support the campaign’s goal.

However, concerning the sports perspective, no consensus has been reached among researchers concerning the motivations for participation in crowdfunding campaigns. To achieve the most consistent results, the authors tend to limit their empirical research to specific crowdfunding models, but their results remain inconsistent with each other (see for instance, multiple research focus on equity model of crowdfunding: Bretschneider & Leimeister, 2017; Cholakova & Clarysse, 2015; Estrin, Gozman, & Khavul, 2018; Gerber & Hui, 2013; Lukkarinen, Wallenius, & Seppälä, 2018). The solution to this challenge could be to focus on projects within a particular model in specific thematic areas, as was done in the football industry, or to divide crowdfunding participants into multiple homogeneous, motivation-based market segments (Feola et al., 2019; Ryu & Kim, 2016).

Considering the abovementioned two captures, in this study, we combine both and state the research question about the heterogeneity of motivations while limiting our insights to the football industry. Hence, this study aims to segment the football club crowdinvestors using investment motivations. To achieve it, the research procedure was based on surveying crowdinvestors of one of the Polish football clubs (Wisla Krakow) and a two-step motivation-based market segmentation technique.

To the best of the author’s knowledge, this is the first crowdfunding-related research that combines the two perspectives presented above. Consequently, the findings contribute to the literature by applying a more fragmented approach to crowdinvestment motivations than that presented. This leads to the verification of the extent to which, in relation to a specific sector, we can find superiority of a given category of motivation, and the extent to which, even in such a strictly defined group, their prioritization will be different. Additionally, the findings provide sports and crowdfunding platform managers with information on the general patterns of football club crowdinvestor-segmentation procedures and outcomes. Based on this study, they could obtain information on who invests in football clubs through crowdfunding campaigns and why they do so. The results presented allow to design marketing communication in a way that the published content corresponds to the values sought by crowdinvestors (resulting from their motivation) as well as to profile who the message should reach (based on segment profiling).

LITERATURE REVIEW

Crowdfunding – the concept, typology, and context of sport

In general, crowdfunding is an open invitation to provide, primarily through the Internet, financial resources to support a project’s campaign as a donation or in exchange for some form of reward (Schwienbacher & Larralde, 2010). In contrast to other forms of financial support, crowdfunding reduces the risk exposure for funders, as they are a large group of individuals providing small amounts of money. In this way, crowdfunding produces the ‘long tail’ of financial services (Haas, Blohm, & Leimeister, 2014), linking the ideas of crowdsourcing and microfinancing together (Mollick, 2014). Consequently, it increases the availability of capital for projects that are often perceived as too risky or not profitable to receive not only a bank loan but also support from business angels or venture capital (Gierczak et al., 2016).

Depending on the reward that the funder receives in return, we can categorize four main crowdfunding models: donation-based, reward-based, lending-based, and equity crowdfunding (Agrawal, Catalini, & Goldfarb, 2013). In donation-based crowdfunding, no material reward is provided. In reward-based, backers received some kind of product, lending-based (crowdlending) is a form of borrowing, while equity crowdfunding (crowdinvesting) provides returns in the form of shares or assets similar to shares.

Regardless of the crowdfunding model, sports projects belong to the most popular thematic category of campaigns (Gałkiewicz & Gałkiewicz, 2018). According to Ratten and Jones (2020), crowdfunding fulfills the second stage of the entrepreneurial ecosystem of sports organizations, such as the start-up stage (the others are: stand up and scale up; Autio et al., 2018), which transforms the initial idea into the potential sports business project. However, the scope of sports crowdfunding campaigns is highly varied and, therefore, it is distinguished into two branches: the crowdfunding of sports, when the creator of the campaign is a sports provider, and sports-related crowdfunding, when a non-sports entity raises money for a sports product (Kościółek, 2021). In crowdfunding of sports, sports clubs are identified as, on the one hand, one of the most common creators of campaigns (Leroux-Sostenes & Bayle, 2019), and on the other hand, objects often included in sports crowdfunding projects (Adam, 2018). Nevertheless, the systematic elaborations on what are the factors that influence the crowdfunding model, as well as what industrial conditions affect the need for crowdfunding in sports organizations, are still lacking.

For professional football clubs, crowdfunding models, such as crowdlending and crowdinvesting, seem to be the most attractive. They can be considered as an alternative to fan bonds and going public, obtaining similar benefits at lower costs of capital, ease and convenience of funding procedures, and deeper informational feedback on the project (Agrawal et al., 2013). In practice, the popularity of these two forms of crowdfunding among football clubs differ across countries. For instance, in Germany, crowdlending is much more popular than crowdinvesting; in Poland, the situation is the opposite (Weimar & Fox, 2021; Kościółek, in press). In this study, conducted in Poland, we thus focus on testing the heterogeneity of investment motivations in equity crowdfunding.

Investment motivations in crowdfunding and within the football industry

The theoretical framework for studies on the identification of motivations among crowdfunding participants is the self-determination theory (SDT). According to SDT, which was developed by Deci and Ryan (2000, 2008), actors engage in specific activities because they are motivated to do so intrinsically, when feeling internal desire for a certain action, or externally, when the reason for the action are rewards, punishments, or other instrumental forms of return. Moreover, such actions meet at least one of the following needs: autonomy, relatedness, and competence. One activity may be accompanied by many specific motivations, but it is important that each of them fit into this framework. This also applies to the crowdfunding participants.

As previously mentioned, there is no consensus among scholars as to which of the class of motivations, intrinsic or extrinsic, is more relevant in the context of crowdfunding participants. In donation-based crowdfunding, donors are motivated both intrinsically and extrinsically (Bagheri, Chitsazan, & Ebrahimi, 2019), mainly by ease of use, perceived self-efficacy, and social connection (Chen et al., 2021). In incentive-based crowdfunding (covering reward-based, lending-based, and equity crowdfunding together), there is an agreement among scholars on the significant role of rewards and financial returns as a motivation for participation in campaigns (Bretschneider & Leimeister, 2017; Cholakova & Clarysse, 2015; Estrin et al., 2018; Gerber & Hui, 2013; Ryu & Kim, 2016), even if such rewards and returns are, as considered by Lukkarinen et al. (2018) the least important motivating factor. Inconsistency in results occurs when examining intrinsic motivations. Cholakova and Clarysse (2015) stated that non-financial motivations have no impact on crowdinvestors, while Gerber and Hui (2013), Bretschneider and Leimeister (2017), and Estrin et al. (2018) found self-image, gaining recognition, and lobbying for certain products, to be equally important to extrinsic motivations.

Faced with these discrepancies, research interest has begun to investigate investment motivations in projects related to specific sectors (Bürger & Kleinert, 2020), including sports (Kościółek, in press). In the case of football clubs, crowdinvestors are fans of the team that creates the campaign (feeling the personal obligation to invest in the club with which they identify), and their motivations are as follows: supporting the cause of a campaign, the status of being a football club owner, rewards, and, to some extent, return on investment.

Crowdinvesting motivations of fans are consistent with what motivates them in related areas such as reward-based crowdfunding and other forms of fan investments. In reward-based crowdfunding, they are fans or family and friends who back the sports club campaigns, for whom both the effects of the support and previous experiences with a club are the most relevant (Huth, 2018a, 2018b; Kościółek, 2021). Taking into account the investigations of the shareholding market, Demir and Rigoni (2017) claimed that football investors are emotionally driven fans who support ‘their’ clubs, while Huth (2020) and Weimar and Fox (2021) proved that traditional investment motivations (including financial returns) for the willingness to invest in sports clubs’ instruments are mainly determined by attitudes and behaviors of club attachment, such as supporting or sympathizing with a club.

As Cocieru, Delia, and Katz (2019) explained, investing in a club is often an expression of fan activism. In a crisis situation, fans feel the need to get involved financially because they feel responsible for the club, as explained by the psychological ownership theory. On the other hand, football club shares do not attract financial-maximizing professional investors as, because of overvaluation, lack of liquidity, and high price volatility (Benkraiem, Le Roy, & Louhichi, 2011; Prigge & Tegtmeier, 2019), these shares do not offer promising returns for them.

Nevertheless, the above-mentioned findings do present aggregated data at the level of the entire population. It still cannot be ruled out that there are crowdinvestors who participate in football clubs’ equity crowdfunding campaigns and who are motivated mostly extrinsically in looking for rewards and return on investment. Therefore, the research question (RQ) is as follows.

RQ) Is motivation among football clubs crowdinvestors homogeneous in

terms of priorities that they give to them?

Market segmentation

The instrumental solution to test investors’ homogeneity is market segmentation, which is the process of dividing the heterogeneous mass market into a homogeneous group of customers (Shank & Lyberger, 2015). Marketing managers put effort into market segmentation to provide the right values to the right target groups by creating the right perception of the product by customers.

The idea of targeting marketing efforts to selected actors in the market was proposed by Frederick (1934) in the 1930s, but Smith (1956) conceptualized market segmentation in the present form we know today. Since then, multiple approaches and segmentation techniques have been proposed. The most relevant distinction is a priori segmentation (called common sense) and post-hoc (called a posteriori) (Dolnicar, 2003, 2008). In a priori segmentation, observations are grouped into ex ante given segments based on theory-driven criteria. In post-hoc segmentation, the segments and classification are estimated using a data-driven approach. Moreover, in post-hoc segmentation, there are two options: one- or two-step procedures; however, it is recommended to use the latter (Tkaczynski, Rundle-Thiele, & Beaumont, 2010). As part of the first step, the segments are estimated with the given sort of variables, and the obtained clusters are profiled with different variables in the second step. The second step has two roles: it deepens knowledge about the segments and validates the segmenting procedure (the segments should differ not only in terms of variables used for clustering).

Taken together, the two-step a priori motivation-based segmentation that is applied in this study is considered to be the most impactful approach, as it leads to finding out who invests in football clubs and why through equity crowdfunding, as well as to provide profiles of given market segments (Dolnicar, 2003; Tkaczynski et al., 2010). In the context of this study, the key point is that this approach leads to the assessment of motivation heterogeneity among crowdinvestors. As a result, it enables the assessment of motivational priorities across market segments and answers the posed research question.

METHODOLOGY

Measurement

Survey research was the method and motivation scale for crowdinvesting in European football clubs (Kościółek, in press) was the instrument used in this study. The scale is based on 17 items belonging to five motivation factors: status of football club ownership (STA: 4 items), fan identification (IDE, 4 items), return on investment (ROI, 4 items), rewards (REW, 3 items), and supporting a cause (SUP, 2 items). The task of the respondents was to assess how much they agreed with the items that were preceded by the sentence “I crowdinvest in [the Club] because…” The level of agreement was measured on a 7-point Likert scale (1 = totally disagree, 7 = totally agree). A list of the items is presented in Table 2.

In addition, the questionnaire included questions to help profile the segments: five measures of consumption behaviors (CON) and five sociodemographic characteristics, such as age, gender, income, place of residence, and marital status. Consumption behaviors were measured on single items, as it is easily interpretable by sports fans (Yoshida, Gordon, Nakazawa, & Biscaia, 2014). Again, they were asked to assess on a 7-point Likert scale how much they agree with performing the following activities ‘very often’: following the news about [the Club] in the media (CON-1), discussing [the Club] with family and friends (CON-2), purchasing [the Club’s] merchandise (CON-3), attending [the Club’s] matches (CON-4) and engaging in [the Club’s] social media (CON-5). Thus, CON-2 measured generating word-of-mouth marketing. All consumption variables have already been used in the literature on sports management (Gray & Wert-Gray, 2012; Kościółek & Nessel, 2019).

Data collection and analysis

The questionnaires were distributed electronically among Wisla Krakow S.A. crowdinvestors, with the assistance of the club’s marketing managers. Wisla Krakow is a Polish football club that remained bankrupt at the beginning of 2019. The club then created an equity crowdfunding campaign and, in a period of less than two hours, it fundraised one million euros (the highest legally allowed amount to be collected through equity crowdfunding in the EU at that time – Sadzius & Sadzius, 2017) from more than 9,000 investors. In March 2020, Wisla increased its capital through crowdfunding. They collected 700,000 EUR from 8,888 investors. Both times, the goal of the campaign was to recapitalize a club in a difficult financial situation and to enable its continued existence in the current legal form (Wisla Krakow, 2019, 2020). In June 2021, each person who invested in Wisla (regardless of which campaign) received an email from the club’s address with a request for participation in the research.

In total, 793 questionnaires were completed (Table 1). The sample was dominated by men (91.9%), people in a marital relationship (74.6%); it composed participants between 30 and 39 years of age (42.9%), and slightly younger (18-29 years: 17.9%) or slightly older (40-49 years: 23.3%). Not much more than half of them (56.0%) have middle-lower incomes as per the Polish standard (under 5,000 PLN ~ 1,250 EUR). More than 70.0% of the crowdinvestors live in Malopolska, the region where the club operates. This means that they have regional connections to the club, assuming that they are Wisla fans.

Table 1. Sample characteristics

|

Characteristics |

n |

% |

Characteristics |

n |

% |

|

Gender |

Age |

||||

|

Female |

64 |

8.07 |

18-29 |

142 |

17.91 |

|

Male |

729 |

91.93 |

30-39 |

340 |

42.88 |

|

Marital status |

40-49 |

185 |

23.33 |

||

|

Single |

201 |

25.35 |

50 and more |

126 |

15.89 |

|

In relation |

592 |

74.65 |

Incomea |

||

|

Place of residence |

2500 and less |

70 |

9.10 |

||

|

Region of the club’s residence |

557 |

70.24 |

2501 - 5 000 |

361 |

46.94 |

|

Outside the region of the club’s residence |

236 |

29.76 |

5000 and more |

338 |

43.95 |

Note: a The number of observations does not sum to the total sample as the answer to this question was not mandatory.

The data analysis comprised three stages, following the most common procedures and techniques for segmenting the market in a two-step approach (Dolnicar, 2003, 2008; Dolnicar et al., 2014; Tkaczynski et al., 2010). First, a confirmatory factor analysis (CFA) was applied to validate the motivation scale. The fitting of empirical data to the factorial structure was verified by the normalized chi-square, comparative fit index (CFI), goodness-of-fit index (GFI), root mean square error of approximation (RMSEA), and normed fit index (NFI). To verify the convergent validity of the scale, the reliability of the factors was assessed using composite reliability (CR) and average extracted variance to verify the convergent validity of the scale (AVE). The acceptable values of all model fit indices were sourced from Hair et al. (2010) and Kline (2005).

Second, cluster analysis was applied to classify crowdinvestors into segments. Despite the common practice of using one-item representatives for a given factor, we followed the approach of Dolnicar et al. (2014) and applied all items to segment the market to avoid losing meaningful variation. The hierarchical Ward method with the Euclidean distance was used to assess the optimal number of segments and, subsequently, the non-parametric k-means method was applied to classify the observations into clusters. Non-parametric Kruskal-Wallis tests and Dunn’s post hoc tests were performed to verify which of the variables (and to what extent) was responsible for the clustering solution and find which segments in pairs differed.

Finally, cluster profiling was performed. Quantitative variables, that is, consumption-related variables, were tested using both Kruskal-Wallis and Dunn’s tests. Qualitative variables, that is, sociodemographic characteristics, were analyzed with chi-squared tests and, if segments differ significantly, Cramér’s V tests show how much their variation is.

RESULTS

Factor analysis

The CFA showed that all constructs, that is, the status of football club ownership (STA), fan identification (IDE), the return on investment (ROI), the rewards (REW), and the support of a cause (SUP) were reliable and valid (Table 2). Factor loadings for all items exceeded the required 0.6 threshold (Hair et al., 2010). The critical ratios for each parameter were statistically significant. The composite reliability was highest for the fan identification (CRIDE = 0.922), slightly lower for the status of football club ownership (CRSTA = 0.861), return on investment (CRROI = 0.849), and rewards (CRREW = 0.846), and the lowest for supporting a cause (CRSUP = 0.662). This means that all of them exceed the required cut-off value of 0.6, which ensures the reliability of these factors (Fornell & Larcker, 1981). The average variance extracted (AVE) also showed acceptable results (> 0.5). One of the factors – supporting a cause (AVESUP = 0.495) – is on the threshold, but since the CR is appropriate, this result can also be accepted, and the entire factorial structure is convergent valid.

The extant model fit was significant (χ2 [df] = 462.596 [109], χ2/df = 4.244, p<0.001), and the model fit indices were RMSEA = 0.064, CFI = 0.952, NFI = 0.939, and GFI = 0.933. The undesirable statistical significance of the model is due to the large sample size for structural modeling, which can be accepted under such conditions. Importantly, all the other indices meet the required criteria: RMSEA < 0.08, CFI > 0.95, NFI > 0.9, and GFI >0.9 (Hair et al., 2010; Kline, 2005).

Table 2. Results of the confirmatory factor analysis

|

|

CR |

AVE |

Factor loading |

S.E. |

C.R. |

M |

SD |

|

Status of a football club owner (STA) |

0.861 |

0.610 |

|||||

|

STA-1: Owning a part of a football clubs is a lot of fun. |

0.880 |

- |

- |

4.45 |

2.17 |

||

|

STA-2: Owning a part of a football club means that my dreams have come true. |

0.841 |

0.035 |

27.929*** |

4.39 |

2.20 |

||

|

STA-3: It feels nice to be a co-owner of the club. |

0.724 |

0.029 |

22.967*** |

5.49 |

1.77 |

||

|

STA-4: I was aiming to obtain the status of the football club owner. |

0.659 |

0.037 |

20.21*** |

4.29 |

2.17 |

||

|

Fan identification (IDE) |

0.922 |

0.748 |

|||||

|

IDE-1: I supported the club that is close to my heart. |

0.923 |

- |

- |

6.68 |

1.00 |

||

|

IDE-2: It is just because I am a fan of this club. |

0.864 |

0.029 |

36.364*** |

6.57 |

1.11 |

||

|

IDE-3: I identify myself with the club. |

0.891 |

0.030 |

38.910*** |

6.46 |

1.19 |

||

|

IDE-4: I care about what will happen with the club. |

0.774 |

0.018 |

28.954*** |

6.79 |

0.62 |

||

|

Return on investment (ROI) |

0.849 |

0.585 |

|||||

|

ROI-1: I can resell these shares for a higher price in the future. |

0.747 |

- |

- |

2.14 |

1.53 |

||

|

ROI-2: My aim is to get a return on my investment. |

0.794 |

0.043 |

21.044*** |

1.85 |

1.30 |

||

|

ROI-3: I think I can earn on these shares someday. |

0.791 |

0.056 |

20.981*** |

2.71 |

1.70 |

||

|

ROI-4: This investment has the potential for a profitable return. |

0.726 |

0.055 |

19.330*** |

2.64 |

1.67 |

||

|

Rewards (REW) |

0.846 |

0.648 |

|||||

|

REW-1: There was a chance to get a unique and attractive reward. |

0.890 |

- |

- |

2.72 |

1.79 |

||

|

REW-2: There was a reward to get in return. |

0.729 |

0.040 |

22.208*** |

3.00 |

1.94 |

||

|

REW-3: I wanted to receive tangible benefits in return for my support. |

0.787 |

0.035 |

24.215*** |

2.42 |

1.73 |

||

|

Supporting a cause (SUP) |

0.662 |

0.495 |

|||||

|

SUP-1: I like the effect that is expected as a result of the campaign. |

0.694 |

- |

- |

6.61 |

0.81 |

||

|

SUP-2: I like the aim of the campaign. |

0.713 |

0.122 |

9.835*** |

6.54 |

0.95 |

Note: CR – Composite Reliability, AVE – Average Variance Extracted, S.E. – Standard Error, C.R. – Critical Ratio, M – Mean, SD – Standard Deviation, *p<0.05; **p<0.01; ***p<0.001.

Based on the mean values, fan identification (M > 6.4) and supporting a cause (M > 6.5) are definitely the predominant motivators for crowdinvestors. The status of football club ownership gives moderate values (M < 4.2), while both rewards, and return on investment are the lowest (≤ 3). All of these were used in the clustering procedure.

Cluster analysis

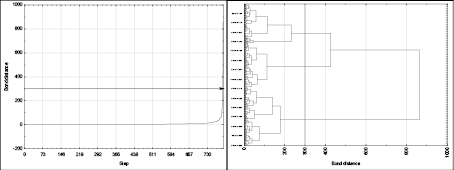

The resulting taxonomy based on Euclidean distance and Ward’s method showed that the first major increment in the cluster dendrogram was above the standardized value of 220. At a distance level of 300, a clear increment was already visible, and hence, the cut-off line was drawn at this point (Figure 1). Three clusters occur at this stage, and this is the number of segments adopted in the subsequent analysis.

Figure 1. Results of the exploratory hierarchical cluster analysis

Therefore, the classification of observations (investors) using the k-means method was carried out for three clusters (segments). The segments shown were not quantitatively balanced (Table 3); Cluster 3 constituted the largest group (50.7% of the market; n = 402), followed by Cluster 1 (45.3%; n = 359), and a small segment of Cluster 2 (4.0%; n = 32).

The two dominant segments in terms of numbers (96% of the market) are concentrated among supporters of the club initiating the campaign (means above 6.50 for each IDE item tested). These two segments are similar in this respect: none of the items describing the fan identification differentiates them (Table 3). In contrast, Cluster 2 differed significantly from them (HIDE-1 = 231.515, HIDE-2 = 184.209, HIDE-3 = 153.004, HPER-4 = 178.435 [p<0.001 for each H]), with lower mean values for all items ( IDE-1 = 2.81, IDE-2 = 2.50, IDE-3 = 2.25, IDE-4 = 4.88).

IDE-1 = 2.81, IDE-2 = 2.50, IDE-3 = 2.25, IDE-4 = 4.88).

Table 3. Results of the k-means cluster analysis

|

Cluster 1: Club-oriented (45.3%) |

Cluster 2: Goal-oriented (4.0%) |

Cluster 3: Benefit-oriented (50.7%) |

H |

|

|

Status of a football club owner (STA) |

||||

|

STA-1 |

3.00a |

3.00a |

5.86 |

336.393*** |

|

STA-2 |

2.97a |

2.94a |

5.77 |

312.976*** |

|

STA-3 |

4.56a |

4.16a |

6.43 |

230.579*** |

|

STA-4 |

2.85a |

3.31a |

5.65 |

317.404*** |

|

Fan identification (IDE) |

||||

|

IDE-1 |

6.84a |

2.81 |

6.85a |

231.515*** |

|

IDE-2 |

6.70a |

2.50 |

6.78a |

184.209*** |

|

IDE-3 |

6.57a |

2.25 |

6.70a |

153.004*** |

|

IDE-4 |

6.83a |

4.88 |

6.91a |

178.435*** |

|

Return on investment (ROI) |

||||

|

ROI-1 |

1.53 |

3.50a |

2.57a |

104.462*** |

|

ROI-2 |

1.23 |

3.13a |

2.31a |

164.295*** |

|

ROI-3 |

1.85 |

3.28a |

3.44a |

181.103*** |

|

ROI-4 |

1.75 |

3.28a |

3.39a |

199.757*** |

|

Supporting a cause (SUP) |

||||

|

SUP-1 |

6.62a |

5.53 |

6.69a |

26.465*** |

|

SUP-2 |

6.61a |

5.31 |

6.57a |

34.375*** |

|

Rewards (REW) |

||||

|

REW-1 |

1.65a |

2.31a |

3.70 |

258.463*** |

|

REW-2 |

1.93a |

2.50a |

4.00 |

229.408*** |

|

REW-3 |

1.49a |

2.03a |

3.28 |

213.800*** |

Note: For each variable (row), the means for different customer segments with the superscript a are not significantly different (p < 0.05) based on Dunn’s multiple comparison tests, *p<0.05; **p<0.01; ***p<0.001.

In addition to the fan identification, Clusters 1 and 3 shared similar levels of motivation to achieve the campaign goal. Equally important to them ( > 6.0) is the effect this can have on the club and the purpose for which the money raised will be used. Compared to these two clusters, investors grouped in Cluster 2 are also significantly less motivated in this regard (HSUP-1 = 26.465, HSUP-2 = 34.375 [p<0.001 for both H]). However, simultaneously, compared to the other dimensions of motivation within this segment, achieving goals is the most important determinant of their campaign participation (SUP-1 = 5.53; SUP-2 = 5.31). Cluster 2 can be called a segment of “goal-oriented” crowdinvestors.

Despite some similarities between Clusters 1 and 3 (in terms of their relationship with the campaign initiator and importance of achieving the campaign goal), there are areas where the two segments differ significantly. This relates to the attitude toward their own profits that their participation in the campaign can bring. These benefits can be seen in three areas: the status of the co-owner of the club (HSTA-1 = 336.393, HSTA-2 = 312.976, HSTA-3 = 230.579, HSTA-4 = 317.404 [p<0.001 for each H]), the return on investment (HROI-1 = 104.462, HROI-2 = 164.295, HROI-3 = 181.103, HROI-4 = 199.757 [p<0.001 for each H]), and the rewards received for the support provided (HREW-1 = 258.463, HREW-2 = 229.408, HREW-3 = 213.800 [p<0.001 for each H]).

For Cluster 1, the importance of the status of the co-owner was rather low (STA-1 = 3.00, STA-2 = 2.97, STA-3 = 4.56, STA-4 = 2.85). This strongly likens this segment to Cluster 2 of goal-oriented investors, with whom it shares a common approach for all items within this dimension. Thus, the role assigned to the status of the club co-owner is a characteristic of Cluster 3. Furthermore, the rewards that could be received for investments motivate them more than investors from the two other clusters (REW-1 = 3.70, REW-2 = 4.00, REW-3 = 3.28). Again, Clusters 2 and 3 do not have statistically significant differences, giving potential personal benefits (here in the prospect of receiving rewards) negligible importance (across all three items for both groups ≤ 2.50). It is not the reward; however, the shares issued are a typical form of return for equity crowdfunding. Unexpectedly, this motivation was found to have the weakest intensity in all three identified segments ( ≤ 3.50). These are crowdinvestors from Cluster 2 and Cluster 3, who present similar intensities of motivation expressing attitude to return on investment, while Cluster 1 has the lowest priority regarding ROI ( < 2.00).

Overall, for most variables (items that form dimensions), one segment differed from the other two, interchangeably representing pairs with consistent motivations. It was also noted that there are two segments with high levels of fan identification, but differing in the importance attributed to the benefits an individual may derive from participating in equity crowdfunding. In contrast to Cluster 1 that group (only) “club-oriented” crowdinvestors, those of Cluster 3 are “benefit-oriented” as they are motivated by returns in the form of club co-ownership status, rewards, and – to a limited extent – by return on investment opportunities. The third segment, Cluster 2, consists of goal-oriented investors and represents a market niche. It is made up of people who have no emotional ties to the campaign’s initiator (fan identification), and their support was motivated primarily by a desire to help the club achieve the campaign’s goal.

Clusters profiling and validation

The results of the discriminant analysis (Table 4) confirmed the consistency of the classification achieved by observations into segments (Rohm, Milne, & McDonald, 2006). The high eigenvalues of the two estimated functions (2.26 and 2.00, respectively) and Wilks’ lambda value confirm the significance of the clustering performed. The classification matrix indicated that 95.80% of all cases could be correctly classified, with the most accurate classification being in the benefit-oriented segment (97.5%). Furthermore, the high (>0.80) canonical correlation values indicate high correlations between discriminant values and segment allocations, ultimately confirming the good fit of the adopted taxonomy with empirical data.

Table 4. Results of the discriminant analysis

|

|

Eigenvalue |

% of variance |

Canonical correlation |

Wilks’ lambda |

chi-square |

df |

p |

|

Function 1 |

2.26 |

53 |

0.83 |

0.10 |

1783.61 |

34 |

<0.001 |

|

Function 2 |

2.00 |

47 |

0.82 |

0.33 |

860.22 |

16 |

<0.001 |

Note: 1-1: 94.4%, 2-2: 90.6%, 3-3: 97.5%, and overall: 95.8% of original cases correctly classified.

Table 5. Consumption-related variability between clusters

|

|

Total |

Cluster 1: Club-oriented (45.3%) |

Cluster 2: Goal-oriented (4.0%) |

Cluster 3: Benefit-oriented (50.7%) |

H |

|

CON-1 |

6.54 |

6.65a |

2.87 |

6.73a |

136.420*** |

|

(1.13) |

(0.83) |

(2.01) |

(0.70) |

||

|

CON-2 |

5.75 |

5.71 |

1.90 |

6.09 |

90.789*** |

|

(1.70) |

(1.64) |

(1.49) |

(1.37) |

||

|

CON-3 |

4.34 |

4.13 |

1.61 |

4.74 |

76.822*** |

|

(1.87) |

(1.89) |

(1.17) |

(1.68) |

||

|

CON-4 |

5.05 |

4.97a |

1.71 |

5.39a |

69.095*** |

|

(2.07) |

(2.10) |

(1.32) |

(1.84) |

||

|

CON-5 |

3.94 |

3.65 |

1.45 |

4.39 |

67.470*** |

|

(2.16) |

(2.21) |

(1.09) |

(2.00) |

Note: *p<0.05; **p<0.01; ***p<0.001.

All the variables related to the level of consumption of sports club products that initiated the equity crowdfunding campaign significantly differentiated the identified market segments (Table 5). This was mainly the case for seeking media information on club-related topics (HCON-1 = 136.420; p < 0.001), generating word-of-mouth marketing about the club (HCON-2 = 90.789; p < 0.001), and the frequency of buying official merchandise (HCON-3 = 76.882; p < 0.001). The separated groups of investors also had different levels of frequency of attending their matches (HCON-4 = 69.095; p < 0.001) and social media engagement with the campaign initiator (HCON-5 = 67.470; p < 0.001).

Unlike purchase motivation, there is no single consumption variable, the intensity of which is the same for any pair of segments. Benefit-oriented investors exhibited the highest levels of consumption intensity in all areas studied. In general, it should be assumed that they show very high levels of interest in the club in the media ( > 6.5), generated word-of-mouth marketing ( > 6.0), have a high frequency of attendance at matches ( > 5.00), and a moderate interest in club merchandise and involvement in social media ( > 4.00). The counterbalance for the described segment is that of goal-oriented investors, who can be considered uninterested in the campaign creator’s products. Excluding interest in the club in the media (CON-1 = 2.87), the averages for all variables describing the consumer behavior of this group were extremely low ( < 2.00).

Unlike gender (χ2 = 1.37; ns.), age (χ2 = 12.21; p < 0.1), marital status (χ2 = 5.34; p < 0.1), monthly income (χ2 = 12.82; p < 0.1), and place of residence (χ2 = 32.60; p < 0.001) were sociodemographic variables that significantly differentiated the identified market segments (Table 6). The magnitude of segment variation within these statistically significant sociodemographic variables was rather low (V < 0.10), with a moderate role for place of residence (V = 0.20).

We can observe the underrepresentation of the youngest crowdinvestors in the “club-oriented” segment (13% vs. 22% in the other two segments) and the overrepresentation of above-average earners in the “goal-oriented” segment (68% vs. 39% and 47% in the other two segments). Additionally, goal-oriented investors are distinguished by their lack of location ties to the club’s headquarters (69% live outside the region). The presence of these differences creates the profiles of the segments and confirms the correctness of the analysis.

Table 6. Socio-demographic variability between clusters

|

Cluster 1: Club-oriented (45.3%) |

Cluster 2: Goal-oriented (4.0%) |

Cluster 3: Benefit-oriented (50.7%) |

Chi-square (Cramer’s V) |

|

|

Age |

12.21* |

|||

|

18-29 |

13% |

22% |

22% |

(0.09) |

|

30-39 |

43% |

34% |

43% |

|

|

40-49 |

25% |

31% |

21% |

|

|

50 and more |

18% |

13% |

14% |

|

|

Gender |

1.37 |

|||

|

Female |

9% |

3% |

7% |

|

|

Male |

91% |

97% |

93% |

|

|

Maritial statusa |

5.34* |

|||

|

Single |

21% |

26% |

29% |

(0.08) |

|

In relation |

79% |

74% |

71% |

|

|

Income |

12.82* |

|||

|

2500 and less |

8% |

10% |

10% |

(0.09) |

|

2501 - 5 000 |

45% |

23% |

51% |

|

|

5000 and more |

47% |

68% |

39% |

|

|

Place of residence |

32.60*** |

|||

|

Region of the club’s residence |

72% |

25% |

72% |

(0.20) |

|

Outside the region of the club’s residence |

28% |

75% |

28% |

Note: a Cluster 2 was not included in chi-square tests due to the low number of observations, *p<0.05; **p<0.01; ***p<0.001.

DISCUSSION AND CONCLUSIONS

This study aims to segment the football club crowdinvestors using investment motivations. In the results of the cluster analysis, we obtained three market segments of crowdinvestors who can be described as follows: (i) benefit-oriented investors with a high level of fan identification that comes from emotional identification with the club, who care about the goal of the campaign, but are also motivated by external benefits in the form of rewards, and the status of being a co-owner of the club; (ii) club-oriented investors for whom the fan identification is predominant and the desire to achieve the goal, while other motivations are secondary; and (iii) goal-oriented – not expecting external benefits, with little emotional connection to the club, but hoping to achieve the goal for which the campaign is being run.

The segmentation criterion was a unique set of motivations related to sports crowdfunding (Kościółek, in press); therefore, it was not possible to compare the results with studies that used the same list of variables. However, in segmentation studies in sports, it is common to adopt the psychological continuum model (PCM) for this purpose (see, e.g., Doyle, Kunkel, & Funk, 2013; Giulianotti, 2002; Park, Kim, & Chiu, 2021; Pu & James, 2017). According to the PCM (Funk & James, 2001), sports club activities go through four successive phases of involvement in its relationship with the fans of the club: awareness, attraction, attachment, and loyalty. In the case of equity crowdfunding campaigns, we found two large market segments (more than 95% of the entire market) with high levels of fan involvement. Therefore, it can be assumed that those involved in equity crowdfunding campaigns are fans at the highest levels of the continuum, that is, attachment and loyalty.

Unlike many segmentation studies on sports fans, analogous research on crowdfunding is scarce. In the Web of Science and Scopus databases, we found only two papers on this topic. First, it relates to the segmentation of crowdinvestors based on decision-making criteria (Feola et al., 2019) and the motivation-based segmentation of backers in reward-based crowdfunding (Ryu & Kim, 2016). From these two perspectives, it is difficult to relate the clustering of crowdfunding equity investors based on the decision criteria to the behavior of crowdinvestors of football clubs, as they are a group of incidental investors (creating a community focused around the fundraising initiator and not around the crowdfunding platform) (Kościółek, in press). This means that they do not make a choice that answers the question “which campaigns to support,” but rather “whether to support the club’s campaign.”

Therefore, in line with analogies to the already known market segments of crowdfunding campaign participants, Ryu and Kim (2016) relate the rewards-based model as a point of reference. Among the four segments distinguished, there were: (i) angelic backers focused on altruistic help, not expecting personal benefits from the support provided; (ii) reward hunters looking for attractive rewards, which on the basis of equity crowdfunding should also be equated with those looking for investment opportunities; (iii) avid fans specific initiators, but also focused on gaining rewards and gaining a position in the community; and (iv) tasteful hermits strongly associated with the initiator (similar to die-hard fans), but they do not give high importance to other potential benefits of participation in the campaign (low level of extrinsic motivation). Based on the characteristics presented, there are great similarities between the pairs of goal-oriented and angelic backers, benefit-oriented and avid fans, and club-oriented and tasteful hermits. However, there is no counterpart to the reward hunters segment among crowdinvestors of football clubs. This shows that, contrary to previous research, the most extrinsically oriented segment was not found among them.

Theoretical contribution

The findings suggest a dominant role for intrinsic motivations among football club crowdinvestors: fan identification, supporting a campaign’s cause, and the status of a football club owner. This supports evidence from previous work in the field of sports crowdfunding (Huth, 2018a, 2018b; Kościółek, 2021, in press) and football fans’ investments (Huth, 2020; Prigge & Tegtmeier, 2020; Weimar & Fox, 2021). According to SDT (Deci & Ryan, 2008), humans are intrinsically driven to satisfy three basic needs: autonomy (i.e., having control), relatedness (refers to having a sense of belonging), and competence (refers to self-efficacy in one’s achievement). In our case, each of the intrinsic motivations relates to different needs: fan identification to the need for relatedness, support of a campaign cause to the need for autonomy, and the status of football clubs to the need for competence. The result of segmentation showed that the need for autonomy is satisfied within all segments, the need for relatedness occurs in the vast majority of crowdinvestors, and the need for competence occurs only for some of them.

Overall, these results shed new light on what we know about crowdinvestor motivations by showing that their mix is quite heterogeneous, even if the scope of the analysis is limited to a homogeneous group of football clubs as campaign creators. However, regarding the categories of motivation, it has been confirmed that within such a narrowly defined group, there is a domination of one of them, in this case, intrinsic motivations.

Practical implications

The adopted two-step motivation-based segmentation makes it possible to provide recommendations to sports managers as to what the appropriate value proposition is for each market segment of football club crowdinvestors.

In respect of the particular segments, the marketing communication of the football club equity crowdfunding campaigns should include the following elements: (i) Club-oriented crowdinvestors – formulating a value proposition based on the collective action of the community for the club, with a clearly stated and universally accepted campaign goal by the community around the club, as well as providing information on moving higher in the internal hierarchy of the club after obtaining the symbolic status of its co-owner; (ii) Benefit-oriented crowdinvestors – the same value propositions as in the case of club-oriented crowdinvestors, as well as: providing attractive rewards with the club’s logo, making a commitment that promotion to the level of club co-owners is associated with receiving confirmation of this fact in the form of a share certificate, declaration of the organization of general meetings, where investors will have the opportunity to make decisions on topics related to the club; (iii) Goal-oriented crowdinvestors – value propositions referring to the importance of the goal being pursued, not only for the club itself, but also for its immediate environment (e.g., the “raison d’état” of given competitions, of which the club is an important part for historical reasons), as the addressee of the proposition in this segment is largely people who are not part of the club’s fan community. This group should also be provided with information on the relationship between the provided support and the possibility of being a co-owner of the club and (optionally) an indication of the opportunity to sell the shares for a profit in the future (if applicable).

The value proposition presented to potential crowdinvestors within each segment is a form of commitment that the club initiating the fundraiser must fulfil. The target effect is customer satisfaction, which builds long-term relationships with customers. While the equity crowdfunding campaign itself can be classified as a one-time purchase product, it is aimed at the existing group of customers of the basic product (club fans), and obtaining and maintaining consumer loyalty to this group is a highly desirable situation.

Limitations and recommendations

As in the case of cultural projects and the reward-based model (Bürger & Kleinert, 2020; Huth, Ryu, & Kim, 2016), equity crowdfunding investors in sports are a heterogeneous group. Therefore, future research should include other sectors to test the robustness of the findings. Moreover, to complete the picture of sports crowdfunding, similar research on motivations and segmentations other than equity crowdfunding models is still necessary.

However, it is worth undertaking these studies in different national and situational contexts, to compare the results of the study coming from a singular Polish club. Despite the fact that both the Polish crowdfunding regulations (Sadzius & Sadzius, 2017) and the financial structures of football clubs (Sports Business Group, 2019) are in line with the main trends in the European market, limiting research to only one football club and the specific cause of campaigns, such as avoidance of the club’s bankruptcy, are the greatest limitations of this study. In future research, it is highly recommended to investigate how the heterogeneity of motivations would differ, when the creator of the campaign has a good financial situation, and the campaign goal is not oriented toward the survival of the club, but its intensive development.

References

Adam, M. C. (2018). Reward or equity crowdfunding in sport related projects. Journal of Sport and Kinetic Movement, I(31), 19–26.

Agrawal, A., Catalini, C., & Goldfarb, A. (2013). Some simple economics of crowdfunding. In Natural Bureau of Economic Research (Vol. 19133). Retrieved from http://www.nber.org/papers/w19133

Ahtiainen, S., & Jarva, H. (2022). Has UEFA’s financial fair play regulation increased football clubs’ profitability? European Sport Management Quarterly, 22(4), 569–587. https://doi.org/10.1080/16184742.2020.1820062

Autio, E., Nambisan, S., Thomas, L. D. W., & Wright, M. (2018). Digital affordances, spatial affordances, and the genesis of entrepreneurial ecosystems. Strategic Entrepreneurship Journal, 12(1), 72–95. https://doi.org/10.1002/sej.1266

Bagheri, A., Chitsazan, H., & Ebrahimi, A. (2019). Crowdfunding motivations: A focus on donors’ perspectives. Technological Forecasting and Social Change, 146, 218–232. https://doi.org/10.1016/j.techfore.2019.05.002

Belleflamme, P., Lambert, T., & Schwienbacher, A. (2014). Crowdfunding: Tapping the right crowd. Journal of Business Venturing, 29(5), 585–609. https://doi.org/10.1016/j.jbusvent.2013.07.003

Benkraiem, R., Le Roy, F., & Louhichi, W. (2011). Sporting performances and the volatility of listed football clubs. International Journal of Sport Finance, 6(4), 283.

Bretschneider, U., & Leimeister, J. M. (2017). Not just an ego trip: Exploring backers’ motivation for funding in incentive-based crowdfunding. Journal of Strategic Information Systems, 26(4), 246–260. https://doi.org/10.1016/j.jsis.2017.02.002

Bürger, T., & Kleinert, S. (2020). Crowdfunding cultural and commercial entrepreneurs: An empirical study on motivation in distinct backer communities. Small Business Economics. https://doi.org/10.1007/s11187-020-00419-8

Chen, Y., Dai, R., Wang, L., Yang, S., Li, Y., & Wei, J. (2021). Exploring donor’s intention in charitable crowdfunding: Intrinsic and extrinsic motivations. Industrial Management & Data Systems. https://doi.org/10.1108/IMDS-11-2020-0631

Cholakova, M., & Clarysse, B. (2015). Does the possibility to make equity investments in crowdfunding projects crowd out reward-based investments? Entrepreneurship Theory and Practice, 39(1), 145–172. https://doi.org/10.1111/etap.12139

Cocieru, O. C., Delia, E. B., & Katz, M. (2019). It’s our club! From supporter psychological ownership to supporter formal ownership. Sport Management Review, 22(3), 322–334. https://doi.org/10.1016/j.smr.2018.04.005

Deci, E. L., & Ryan, R. M. (2008). Self-determination theory: A macrotheory of human motivation, development, and health. Canadian Psychology, 49(3), 182–185. https://doi.org/10.1037/a0012801

Demir, E., & Rigoni, U. (2017). You lose, i feel better: rivalry between soccer teams and the impact of schadenfreude on stock market. Journal of Sports Economics, 18(1), 58–76. https://doi.org/10.1177/1527002514551801

Dolnicar, S. (2003). A review of unquestioned standards in using cluster analysis for data-driven market segmentation. Australasian Journal of Market Research, 2002(December), 2–4.

Dolnicar, S. (2008). Market segmentation in tourism. In A.G. Woodside & D. Martin (Eds), Tourism Management: Analysis, Behaviour and Strategy (pp. 129–150). Wallingford: CAB International.

Dolnicar, S., Grün, B., Leisch, F., & Schmidt, K. (2014). Required sample sizes for data-driven market segmentation analyses in tourism. Journal of Travel Research, 53(3), 296–306. https://doi.org/10.1177/0047287513496475

Doyle, J. P., Kunkel, T., & Funk, D. C. (2013). Sports spectator segmentation: Examining the differing psychological connections among spectators of leagues and teams. International Journal of Sports Marketing and Sponsorship, 15, 95–111. https://doi.org/10.1108/IJSMS-14-02-2013-B003

Estrin, S., Gozman, D., & Khavul, S. (2018). The evolution and adoption of equity crowdfunding: Entrepreneur and investor entry into a new market. Small Business Economics, 51(2), 425–439. https://doi.org/10.1007/s11187-018-0009-5

Feola, R., Vesci, M., Marinato, E., & Parente, R. (2019). Segmenting “digital investors”: Evidence from the Italian equity crowdfunding market. Small Business Economics, 1–16. https://doi.org/10.1007/s11187-019-00265-3

Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

Frederick, J. H. (1934). Industrial Marketing. Hoboken, New Jersey: Prentice-Hall.

Funk, D. C., & James, J. (2001). The psychological continuum model: A conceptual framework for understanding an individual’s psychological connection to sport. Sport Management Review, 4(2), 119–150. https://doi.org/10.1016/S1441-3523(01)70072-1

Gałkiewicz, D. P., Gałkiewicz, M. (2018). Crowdfunding Monitor 2018: An Overview of European Projects Financed on Startnext and Kickstarter Platforms between 2010 and mid-2017. Retrieved from file:///C:/Users/panda/Downloads/Crowdfunding_Monitor_2018 (1).pdf

Gerber, E. M., & Hui, J. (2013). Crowdfunding: Motivations and deterrents for participation. ACM Transactions on Computer-Human Interaction, 20(6), 1-32. https://doi.org/10.1145/2530540

Gierczak, M. M., Bretschneider, U., Haas, P., Blohm, I., & Leimeister, J. M. (2016). Crowdfunding: Outlining the new era of fundraising. In D. Brüntje & O. Gajda (Eds.), Crowdfunding in Europe (pp. 7–23). Cham: Springer.

Giulianotti, R. (2002). Supporters, followers, fans, and flaneurs. Journal of Sport & Social Issues, 26(1), 25–46. https://doi.org/10.1177/0193723502261003

Gray, G. T., & Wert-Gray, S. (2012). Customer retention in sports organization marketing: Examining the impact of team identification and satisfaction with team performance. International Journal of Consumer Studies, 36(3), 275–281. https://doi.org/10.1111/j.1470-6431.2011.00999.x

Haas, P., Blohm, I., & Leimeister, J. M. (2014). An empirical taxonomy of crowdfunding intermediaries. Thirty Fifth International Conference on Information Systems, 1–18.

Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2010). Multivariate Data Analysis: Global Edition. Upper Saddle River, NJ: Pearson Higher Education.

Huth, C. (2018a). Back to traditional stadium names: Fans’ role in financing naming rights through crowdfunding. Sport, Business and Management: An International Journal, 8(3), 214–234. https://doi.org/10.1108/SBM-05-2017-0027

Huth, C. (2018b). Crowdfunding in sports. German Journal of Exercise and Sport Research, 48(2), 293–298. https://doi.org/10.1007/s12662-018-0512-5

Huth, C. (2020). Who invests in financial instruments of sport clubs ? An empirical analysis of actual and potential individual investors of professional European football clubs. European Sport Management Quarterly, 20(4), 500–519. https://doi.org/10.1080/16184742.2019.1684539

Kline, T. (2005). Psychological Testing: A Practical Approach to Design and Evaluation. Thousand Oaks: Sage.

Kościółek, S. (2021). Backers’ motivations in sports clubs reward-based crowdfunding campaigns. Journal of Physical Education and Sport, 21(Supplement 2), 1165–1171. https://doi.org/10.7752/jpes.2021.s2147

Kościółek, S. (in press). Motivations for crowdinvesting in European football clubs. Journal of Sport Management.

Kościółek, S., & Nessel, K. (2019). Market segmentation of football fans in Poland. In J. J. Zhang & B. G. Pitts (Eds.), Globalized Sport Management in Diverse Cultural Contexts (pp. 154–176). New York: Routledge.

Kozioł-Nadolna, K. (2016). Funding innovation in Poland through crowdfunding. Journal of Entrepreneurship, Management and Innovation, 12(3), 7–29. https://doi.org//10.7341/20161231

Leboeuf, G., & Schwienbacher, A. (2018). Crowdfunding as a new financing tool. In D. Cumming & L. Hornuf (Eds.), The Economics of Crowdfunding: Startups, Portals, and Investor Behavior (pp. 11–28). Cham: Springer.

Leroux-Sostenes, M.-J., & Bayle, E. (2019). The crowdfunding of sport – paving the way to shared sponsorship ? Current Issues in Sport Science, 4, 1–10. https://doi.org/10.15203/CISS

Lukkarinen, A., Wallenius, J., & Seppälä, T. (2018). Investor motivations and decision criteria in equity crowdfunding. SSRN Electronic Journal, 11, 1–44. https://doi.org/10.2139/ssrn.3263434

Mollick, E. (2014). The dynamics of crowdfunding: An exploratory study. Journal of Business Venturing, 29(1), 1–16. https://doi.org/10.1016/j.jbusvent.2013.06.005

Mullin, B. J., Hardy, S., & Sutton, W. (2014). Sport Marketing 4th Edition. Champaign: Human Kinetics.

Nessel, K., Havran, Z., & Máté, T. (2022). Heterogeneity of budget constraints in Hungarian and Polish football. In R. K. Storm, K. Nielsen, & Z. Havran (Eds.), Professional Team Sports and the Soft Budget Constraint (pp. 103–129). Cheltenham: Edward Elgar Publishing.

Park, S., Kim, S., & Chiu, W. (2021). Segmenting sport fans by eFANgelism: A cluster analysis of South Korean soccer fans. Managing Sport and Leisure, 1–15. https://doi.org/10.1080/23750472.2021.1873169

Perechuda, I. (2020). Football clubs drowned by player. Polish Journal of Sport and Tourism, 27(1), 28–32. https://doi.org/10.2478/pjst-2020-0005

Prigge, S., & Tegtmeier, L. (2019). Market valuation and risk profile of listed European football clubs. Sport, Business and Management: An International Journal, 9(2), 146–163. https://doi.org/10.1108/SBM-04-2018-0033

Prigge, S., & Tegtmeier, L. (2020). Football stocks: A new asset class attractive to institutional investors? Empirical results and impulses for researching investor motivations beyond return. Sport, Business and Management: An International Journal, 10(4), 471–494. https://doi.org/10.1108/SBM-07-2019-0063

Pu, H., & James, J. (2017). The distant fan segment: Exploring motives and psychological connection of International National Basketball Association fans. International Journal of Sports Marketing and Sponsorship, 18(4), 418–438. https://doi.org/10.1108/IJSMS-05-2016-0022

Ratten, V., & Jones, P. (2020). New challenges in sport entrepreneurship for value creation. International Entrepreneurship and Management Journal, 16(4), 961–980. https://doi.org/10.1007/s11365-020-00664-z

Rohm, A. J., Milne, G. R., & McDonald, M. A. (2006). A mixed-method approach for developing market segmentation typologies in the sports industry. Sport Marketing Quarterly, 15(1), 29–39.

Ryan, R. M., & Deci, E. L. (2000). Self-determination theory and the facilitation of intrinsic motivation, social development, and well-being. American Psychologist, 55(1), 68–78. https://doi.org/10.1037110003-066X.55.1.68

Ryu, S., & Kim, Y. (2016). Electronic commerce research and applications a typology of crowdfunding sponsors: Birds of a feather flock together ? Electronic Commerce Research and Applications, 16, 43–54. https://doi.org/10.1016/j.elerap.2016.01.006

Sadzius, L., & Sadzius, T. (2017). Existing legal issues for crowdfunding regulation in European Union member. International Journal of Business, Humanities and Technology, 7(3), 52–62.

Schwienbacher, A., & Larralde, B. (2010). Crowdfunding of small entrepreneurial ventures. In D. Cumming (Ed.), The Oxford Handbook of Entrepreneurial Finance (pp. 369–391). Oxford: Oxford University Press.

Shank, M. D., & Lyberger, M. R. (2015). Sports Marketing. A Strategic Perspective (5th ed.). London and New York: Routledge.

Smith, W. R. (1956). Product differentiation and market segmentation as alternative marketing strategies. Journal of Marketing, 21(1), 3–8.

Sports Business Group. (2019). World in motion. Annual Review of Football Finance 2019. Manchester.

Tkaczynski, A., Rundle-Thiele, S., & Beaumont, N. (2010). Destination Segmentation: A recommended two-step approach. Journal of Travel Research, 49(2), 139–152. https://doi.org/10.1177/0047287509336470

Toften, K., & Hammervoll, T. (2009). Niche firms and marketing strategy. European Journal of Marketing, 43(11/12), 1378–1391. https://doi.org/10.1108/03090560910989948

Weimar, D., & Fox, A. (2021). Fan involvement and unusual investor behavior: Evidence from a football fan bond. International Journal of Sport Finance, 16(2), 16–32. https://doi.org/10.32731/ijsf/161.022020.02

Wisla Krakow. (2020). Nigdy Nie Zginie. Retrieved from Beesfund.com website: https://beesfund.com/p/wislakrakow

Wisła Kraków. (2019). Moja Wisła. Strona inwestycji. Retrieved from Beesfund.com website: https://wisla.beesfund.com/

Yoshida, M., Gordon, B., Nakazawa, M., & Biscaia, R. (2014). Conceptualization and measurement of fan engagement: Empirical evidence from a professional sport context. Journal of Sport Management, 28(4), 399–417. https://doi.org/10.1123/jsm.2013-0199

Abstrakt

CEL: Ponieważ kwestia motywacji inwestorów społecznościowych jest nadal przedmiotem intensywnej debaty, w badaniach empirycznych tej kwestii zaczęto skupiać się na określonych branżach oraz heterogeniczności motywacji w ramach określonych modeli finansowania społecznościowego. W niniejszym opracowaniu te dwie perspektywy zostały połączone. W związku z tym rozważane jest pytanie badawcze o niejednorodność motywacji inwestorów społecznościowych klubów piłkarskich. Celem badania jest segmentacja tych inwestorów przy użyciu ich motywacji inwestycyjnych. METODYKA: W badaniu zastosowano metodę sondażu na grupie inwestorów społecznościowych klubu piłkarskiego Wisła Kraków (n = 793) oraz podejście dwustopniowej segmentacji post hoc opartej na motywacjach. Jako że to przedstawiciele klubu prowadzili w lipcu 2021 roku elektroniczną dystrybucję ankiet wśród wszystkich jego inwestorów społecznościowy, wykorzystany dobór próby był doborem wygodnym. Do segmentacji rynku zastosowano analizę skupień, w tym metodę Warda z odległością euklidesową oraz nieparametryczną metodę k-średnich. Różnice między segmentami określano testami chi-kwadrat dla zmiennych jakościowych oraz testami H Kruskala-Wallisa wraz z testami post hoc Dunna dla zmiennych ilościowych. Analiza dyskryminacyjna skutecznie zweryfikowała procedurę segmentacji. WYNIKI: Inwestorzy społecznościowi klubów piłkarskich dzielą się na trzy segmenty rynku: zorientowanych na korzyści (50,7%), zorientowanych na klub (45,3%) i zorientowanych na cel (4,0%). Na takie grupowanie miały wpływ wszystkie wcześniej zidentyfikowane motywacje: identyfikacja fanów, wspieranie celu kampanii, status właściciela klubu piłkarskiego, nagrody i zwrot z inwestycji. Segmenty były również zróżnicowane pod względem zachowań konsumpcyjnych (konsumpcja mediów, marketing szeptany, zakupy produktów klubowych, frekwencja na meczach i zaangażowanie w mediach społecznościowych) oraz profili społeczno-demograficznych (wiek, stan cywilny, dochód i miejsce zamieszkania). Z wyjątkiem niszy zorientowanej na cele, inwestorzy społecznościowi klubów piłkarskich to wysoce zidentyfikowani kibice, którzy są skoncentrowani na wspieraniu celu kampanii. Niektórzy z nich („zorientowani na korzyści”) są przy tym bardziej wrażliwi na status właścicielski klubu, zwrot z inwestycji i nagrody niż pozostali („zorientowanie na klub”). Inwestorzy skupieni na korzyściach w największym stopniu konsumują produkty klubu, podczas gdy zorientowani na cele wręcz przeciwnie. IMPLIKACJE: Opierając się na teorii autodeterminacji, nie znaleziono zgrupowania z przewagą motywacji zewnętrznych. Wyniki te są sprzeczne z większością badań dotyczących finansowania społecznościowego, ale są zgodne z literaturą dotyczącą zarządzania w sporcie. Co ważne, dostarczono dowody na to, że jednorodna grupa pod względem aktywności w zakresie inwestowania społecznościowego może nadal być niejednorodna pod względem motywacji. Wynikającą z tego kontrybucją teoretyczną tego jest spostrzeżenie, że rozumienie motywacji do inwestowania społecznościowego powinno być rozpatrywane w sposób bardziej szczegółowy niż dotychczas. Potwierdziły się również założenia o zaspokajaniu wielu potrzeb jednocześnie w ramach zjawiska inwestowania społecznościowego w kluby piłkarskie. Menedżerom sportowym wyniki te dostarczają informacji na temat segmentów rynku inwestorów społecznościowych, co umożliwia skuteczniejszą komunikację kampanii crowdfundingowych. ORYGINALNOŚĆ I WARTOŚĆ: Niniejsze badanie jest pierwszym, w którym testowano badawczo heterogeniczność motywacji inwestycyjnych wśród inwestorów skupionych wokół klubów piłkarskich. W efekcie wykazano niestabilność wyników badań skoncentrowanych na całych modelach finansowania społecznościowego, które pomijały specyfikę branżową i wewnętrzną różnorodność inwestorów społecznościowych. Ponadto rozszerzono obszar badań nad kibicami inwestorami w branży piłkarskiej, gdyż do tej pory skupiano się na motywacjach inwestorów bez uwzględniania ich wewnętrznej heterogeniczności.

Słowa kluczowe: crowdfunding udziałowy, fani inwestorzy, identyfikacja z drużyną, kluby sportowe, segmentacja rynku, teoria autodeterminacji

Biographical note

Szczepan Kościółek is a Research and Teaching Assistant at the Institute of Entrepreneurship of Jagiellonian University, Poland. His research interests include both sports economics and sport management, specifically the areas of sectoral policies, competitiveness, and consumer behavior.

Conflicts of interest

The author declares no conflict of interest.

Citation (APA Style)

Kościółek, S. (2022). Heterogeneity of motivations among crowdinvestors: Evidence from the football industry. Journal of Entrepreneurship, Management, and Innovation, 18(4), 157-183. https://doi.org/10.7341/20221845